We can explain the meaning of management accounting as the science in which accounting information are collected and analyzed. After this, these information are provided to management for creation of policies and decision making.

According to Anglo American Council on Productivity

From above meaning, we find that management accounting is combination of two words, one is management and other is accounting.

Management means decision making.

But Question is more important than meaning of management

How does manager take decision?

Accounting means resource of accounting date.

But, Question is more important that meaning of accounting

Why does Accountant do hard work day and night for recording and analysis of financial transactions?

Both above two questions are inter-related and invention of management might happen due to the finding answer of above two question

Ans of 1st question : Manager can take the decision with accounting information.

Ans. of 2nd question : Accountant do hard work for providing help to management of company.

After this following Cycle will start

Raw data

↓

↓

Financial Accounting + Cost accounting

↓

↓

Useful Data

↓

↓

→→ Management Accounting →→ Decision Making

So, it is concerned with accounting information that is useful to management. Management accounting's latest research was started since 1950 and after 60 years, its research has reached at the top level and financial statement analysis, ratio analysis, fund flow analysis, cash flow analysis, working capital analysis, investment analysis etc. are its main technique to analyze company and its income and financial position and on these basis, management takes the decision whether company invest his money in that particular company or not.

In simple words, any form of accounting enables business to be conducted more efficiently can regarded as management accounting.

Nature of management accounting guides to know main characteristics of management accounting. Following are main points which shows the nature of management accounting:

1. No Fixed Norms Followed

In financial accounting, we follow different norms and rules for creating ledgers and other account books. But there is no need to follow fixed norms in management accounting. Management accounting tool may be different from one organization to other organization. Using of different tools of management accounting is fully dependent on the persons who are using it. So, business policy of each organization affects rules and regulation of applying management accounting.

2. Increase in Efficiency

It is the nature of management accounting that it is used for increasing in the efficiency of organization. It scans the points of inefficiency through analysis of accounting information. By taking action for improving, organization can increase the efficiency.

3. Supplies Information not Decisions

Management accountant supplies accounting facts and information and also provides interpretation, but decision making is fully dependent on higher authorities. Management accounting is just guide.

4. Concerned with Forecasting

4. Concerned with Forecasting

It is the temperament of management accounting that it is fully concerned with forecasting. In management accounting, historical accounting information is analyzed through common size financial statement, ratio analysis, fund flow analysis and accounting data tendency for knowing the probability of next fact. So, all these things are especially useful for forecasting.

These forecasting may be related with following things

a) sales forecasting

b) production forecasting

c) earning forecasting

d) cost forecasting

SCOPE:

Management Accounting Scope can be divided in following three parts

1. Analysis of Financial Statements Scope

2. Interpretation Scope

3. Decision Making Scope

Now we explain all above parts with more detail.

1. Analysis of Financial Statements/Accounting Data Scope

This part of management accounting scope answers our following questions

Q:- Which tools are being used for analyzing of accounting data?

Q:- Which specific accounting data is used for analyzing financial position, income position and solvency position?

Q:- What are main types of financial statement analysis?

Q:- What are the limitations of financial statement analysis?

2. Interpretation Scope

After analysis through ratio analysis, fund flow analysis, cash flow analysis or any other tool of management accounting, our next management accounting scope is interpretation scope. Analyzed data is also no tongue if you have no idea how to explain it? So, this is big scope for every wise man. Same analyzed financial statement's meaning may be different if interpretation is given by different account managers. For example, If we open the financial statement of twelve five years plan and we find that govt of India paid 1,10,000 Crores rupees for ending of poverty and you can find different detail of it. But if new account manager links it with no. of poor people, then we can see still 85% persons are poor. So, meaning of spending of Rs. 1,10,000 crores will become opposite. So, interpretation is important part of management accounting scope.

3. Decision Making Scope

"Who and how is the accounting information used for decision making?", is the part of scope of management accounting.

FUNCTIONS OF MGT ACCOUNTING:

Management accounting is one of important part of accounting. To use accounting for decision making encourages its development. Management accounting’s main function is to collect accounting information which is useful for different managerial functions like planning, organization, coordination and control. Now, we are explaining other important functions of management accounting.

1st Planning and Forecasting Function:

In 2005, Mr. A started his small business. He was well educated of management accounting tools. By effective use of management accounting, he developed his small business. Now, after 5 years, he is operating good company. Management accounting’s basic functions like to study ratio analysis and cash and fund flow statements can develop any small business like Mr. A. How is it possible?

One – Businessman can easily watch in which project he invested his cash and fund. He can see whether its ROI and ROE is better than any other investment.

Second – He also makes good plan to reduce his investment in that project whose return is not sufficient.

2nd Modification of Data Function:

Second good function of management accounting is to modify of raw accounting data. After this, businessman bids fair to effective use these modify data in business’s management. Management accounting can be used to classify every accounting item in different views. There are so many accounting software which can be helpful to show sale or purchase or any other accounting items according to production level, area, season, country, age or quality of debtors or creditors.

One Side, it will build up analytic approach of company and other side, it will be helpful to check up each and every accounting item from different angels.

3rd Interpretation Function:

It is also function of management accounting to do complete interpretation of financial analysis. It cuts down work burden of manager because management accountant supports him by providing fact and interpretation of financial data after its analysis.

4th Management Control Function:

Management control can be possible only with management accounting function. Management accounting uses responsibility accounting tool in which different cost, revenue and investment centers are made. Proper budget is maintained in each centre. Analysis of actual recorded performance is compared with standard performance and deviation is evaluated. This will be helpful to fix up wrong side of company’s decision promptly. Thus company can do smoothly management control.

5th Communication Function:

Management accounting puts together all useful accounting information with comparable past data for good communication with govt., bankers and investors.

ADVANTAGES OF MA:

Today, we will make clear the advantages of management accounting. After reading this, you will surely study all concepts of management accounting more deeply for becoming perfect in it.

Management accounting is needed in business because it has capacity to change the business performance and financial position. Please pay attention to the advantages of management accounting.

1st : Increase Efficiency :

Management accounting increases the efficiency of operation of company. Everything is done in management accounting with a scientific system for evaluating and comparing the performance. With this, we find deviations. We will take promotional decisions on this basis. Other employees will also be motivated with this because if their performance will be favourable, they get reward of this. Thus management accounting increases efficiency.

2nd : Maximizing the Profitability :

Using of management accounting's budgetary control and capital budgeting tool, company can easily succeed to reduce both operating and capital expenditures. After this, company can reduce its price and then company will receive super profits.

3rd : Simplify the Financial Statements

For taking different managerial decisions, management accountant provides deep technical reports with simple interpretations in which he mentions the facts of financial statements, after this, company's management officers understand what is in financial statement and how will they use this for company's progress.

4th : Control of Business's Cash Flow :

It is one of important advantage of management accounting that it can be used for controlling of business's cash flow. We all know that cash in hand is better than in fixed properties if there is emergency to pay our loan or debt. So, management accountant deeply studies from where is money coming and where is it going. To check on misuse of money will surely control of business's cash flow.

5th : Business-critical Decisions

To take business - critical decisions, now management accounting will become more powerful. Global management accountants are coming for join on one plate-form for taking all business critical decisions.

TOOLS OF MA:

In previous educational contents, we've explained functions and advantages of management accounting. Both contents were published to tell the importance of this branch of accounting. We want to take this conversation a step further today, and discuss tools and techniques of management accounting that can be helpful to management for providing best information. Take a look at some of best tools and techniques of management accounting outlined below:

1st Tool : Analysis of Financial Statements

Analysis of financial statements is the main tool of management accounting. In this tool, we collect four financial statement, one is profit and loss account, second is balance sheet, third is cash flow statement and fourth and last is fund flow statement. After this, we calculate more than 30 ratios and also analyze the financial statement by financial analysis, fund flow analysis and cash flow analysis. Main aims of analysis of financial statements are following :

1. Profitability - its ability to earn income and sustain growth in both short-term and long-term. A company's degree of profitability is usually based on the income statement, whichreports on the company's results of operations;

2. Solvency - its ability to pay its obligation to creditors and other third parties in the long-term;

3. Liquidity - its ability to maintain positive cash flow, while satisfying immediate obligations;

Both 2 and 3 are based on the company's balance sheet, which indicates the financial condition of a business as of a given point in time.

4. Stability- the firm's ability to remain in business in the long run, without having to sustain significant losses in the conduct of its business. Assessing a company's stability requires the use of both the income statement and the balance sheet, as well as other financial and non-financial indicators.

2nd Tool : Budgetary Control

This is that tool of management accounting in which we make budgets for planning and control of fund. All budgets are made with past historical accounting data and future expectations. After this budgeted data is compared with actual recorded accounting data and performance is calculated on the basis of deviation between actual and expected performance.

3rd Tool : Decision Accounting

There are lots of decision which businessman has to take on the basis of tools of management accounting. One of management accounting tool is decision accounting. It is helpful to take main decision which we can explain following ways :

a) To Buy or to construct any fixed asset

b) Do's or Dont's to do any business activity

c) To choose best alternative

d) Calculation the price of product

4th Tool : Throughput accounting

4th Tool : Throughput accounting

Throughput Accounting (TA) is a dynamic, integrated, principle-based, and comprehensive management accounting's tool that provides managers with decision support information for enterprise optimization. Actually this is the extension of decision accounting. Throughput accounting is relatively new in management accounting. It is an approach that identifies factors that limit an organization from reaching its goal, and then focuses on simple measures that drive behavior in key areas towards reaching organizational goals.

5th Tool : MIS

We MIS tool, management accountant provides information needed to manage organizations effectively

. If we have to understand MIS, we need to understand ERP, SCM, CRM, DSS and other computer techniques for providing information with effective ways.

6th Tool : Financial Policy

Financial policy is that tool of management accounting which is needed to make good structure of capital mix We decide the proportion of share capital and loans in capital structure. Financial and operating leverages are also its sub-tools.

7th Tool : Working Capital Management

With this tool of management accounting, we manage short term assets and short term liabilities. All cash management, debtor management and inventory management will include in working capital management. We make also working capital cycle for knowing the firm's ability to convert its resources into cash. If there is low time for conversion of raw material into sales and then cash from debtor, it is good indication.

DIFF BETWEEN FINANCIAL ACCOUNTS AND MANAGEMENT ACCOUNTS:

Financial Accounting and Management accounting both are the main branches of Accounting. Both are very necessary for better business decision. All the data which is used in management accounting are taken from financial accounting. But there are many difference between financial accounting and management accounting.

Following are the main differences of financial accounting and management accounting :-

Financial Accounting Vs Cost Accounting

Both cost accounting and financial accounting are the parts of accounting. Both provide useful information to the businessman for decision making. Both can be used for reducing cost and increasing the profit and wealth of business. But there are lots of differences between cost accounting and financial accounting. Financial accounting provides the information of expenses on the basis of historical transactions. In cost accounting, we show the detailed information of expenses.

For example: We have 5 products. Financial accounting's income statement will show just the total material cost, direct expenses, indirect expenses, sale and net profit but it will not show the each product's material cost, labour cost, overhead cost, sale and net profit. All these information can be obtained through cost accounting.

Now, we are explaining the differences between cost accounting and financial accounting.

1. Meaning

Cost Accounting : Cost accounting is that part of accounting which is helpful to calculate the cost and control the cost. In cost accounting, we deeply study the variable cost, fixed cost, overheads and capital cost.

Financial Accounting : Financial Accounting is that part of accounting in which we record the transactions and we make the financial statements. Through making the financial statement, it provide information of profitability and financial position to the interested parties.

2. Objective

Cost Accounting : We can not take all decisions on the basis of information which have been provided by financial accounting. After making the financial statements under financial accounting, we calculate the cost of each unit and use the techniques of cost accounting for better decision making.

Financial Accounting : Main objective of financial accounting is to show the financial statement correctly.

3. Law

Cost Accounting : There is not any restriction on the cost accounts. It can be made according to the need of company but some company must audit their cost accounts under cost audit.

Financial Accounting : In financial accounting, there are lots of law restrictions. For example, company accounts and financial statements must be according to the format of company law. It should also follow the rules of IFRS and income tax law.

4. Controlling

Cost Accounting : In cost accounting, we study the techniques of controlling the cost. All the costs are calculated for the purpose of controlling the cost. For example, Company produces product A, B and C. If product C is generating 30% but product A and B is generating just 5%. We will try to control the cost of A and B product through different techniques of cost control.

Financial Accounting : In financial accounting, we just record the transactions correctly. We do not care to control the cost.

5. Profit Analysis

Cost Accounting : In cost accounting, to find the profit per job or per batch or per service unit is possible.

Financial Accounting : In financial accounting. we make the income statement which shows the net profit or loss or whole organisation not one job or batch.

6. Record

Cost Accounting : In cost accounting, both actual transactions record and estimations are used. For example budgetary control and variance analysis, we set the standard cost which is based on the estimations. These estimations may be differ from actual cost.

Financial Accounting : In financial accounting, we use actual transaction for recording purpose. We do not use the estimation for preparing income statements and balance sheet.

7. Valuation of Inventory

Cost Accounting : In cost accounting, inventory's valuation will be on cost.

Financial Accounting : In financial accounting, inventory's valuation will be on the cost or market value which will be low.

8. Cycle

Cost Accounting : In cost accounting, we first calculate the raw material cost. Then, we calculate the labour cost. Then, we calculate the direct material cost. After this, we calculate the overhead cost. All these cost are added. A profit margin is added. An estimated sale price is calculated. Its whole controlling cycle will be relating to control the cost of raw material, labour cost and overheads.

Financial Accounting : In financial accounting, we pass the journal entries. Then, we make the ledger accounts. Then, we prepare the trial balance. Then, we make the final accounts.

FINANCIAL STATEMENTS:

Financial statements are the final product of accounting and these statements show the balance sheet and profit and loss account of company. Financial statements are the base of decisions which are taken by management of company and other interested parties. All other interested parties include investors, creditors, customers, employees, future investors, government and public. They take decisions according to the results of these financial statements.

Features of Financial Statements

1. Recorded Facts

It is the feature of financial statements that it is based on recorded facts. We record daily transactions relating to cash, bank, purchase, sale and many others. All these transactions are recorded on the historical cost or revenue. So, financial statement shows only book value of assets, liabilities, incomes and expenditures.

2. Accounting Conventions

For making financial statements, we use some of accounting conventions. These conventions are useful for making financial statements more comparable, easy and real.

3. Accounting assumptions

For making financial statements, we accept going concern and measurement in money assumption.

4. Personal Judgment

Personal judgment is very important in making of financial statement. For example, if we use FIFO for valuation of inventory, our financial statements show result according to this judgment and it will different if we use LIFO for valuation of inventory. There are many other valuation methods and one of these; we have to apply in accounting. Except these, there are many other decisions affect financial statements.

Types of Financial Statement

1. Balance Sheet

2. Profit and Loss Account

3. Profit and Loss Appropriation Account

3. Fund Flow Statement

4. Cash Flow Statement

BALANCE SHEET:

I) Goodwill

II) Patents

III) Trade marks and design

Depreciation is charged on every fixed asset except land, because value of land will increase after some time. Here, students are given advice that they should calculate the value of net fixed assets, if different fixed assets are purchased or sold during the year. The following table will be the part of working note.

4. Miscellaneous expenditures

In share capital of company, we have to show authorized capital, subscribed capital, called up capital and paid up capital. For calculating paid up capital, we will deduct calls unpaid and add original paid up amount offorfeited shares.

According to Anglo American Council on Productivity

" Management accounting is the presentation of accounting information in such a way to assist management in creation of policy and day to day operation of an undertaking."

From above meaning, we find that management accounting is combination of two words, one is management and other is accounting.

Management means decision making.

But Question is more important than meaning of management

How does manager take decision?

Accounting means resource of accounting date.

But, Question is more important that meaning of accounting

Why does Accountant do hard work day and night for recording and analysis of financial transactions?

Both above two questions are inter-related and invention of management might happen due to the finding answer of above two question

Ans of 1st question : Manager can take the decision with accounting information.

Ans. of 2nd question : Accountant do hard work for providing help to management of company.

After this following Cycle will start

Raw data

↓

↓

Financial Accounting + Cost accounting

↓

↓

Useful Data

↓

↓

→→ Management Accounting →→ Decision Making

So, it is concerned with accounting information that is useful to management. Management accounting's latest research was started since 1950 and after 60 years, its research has reached at the top level and financial statement analysis, ratio analysis, fund flow analysis, cash flow analysis, working capital analysis, investment analysis etc. are its main technique to analyze company and its income and financial position and on these basis, management takes the decision whether company invest his money in that particular company or not.

In simple words, any form of accounting enables business to be conducted more efficiently can regarded as management accounting.

Nature of management accounting guides to know main characteristics of management accounting. Following are main points which shows the nature of management accounting:

1. No Fixed Norms Followed

In financial accounting, we follow different norms and rules for creating ledgers and other account books. But there is no need to follow fixed norms in management accounting. Management accounting tool may be different from one organization to other organization. Using of different tools of management accounting is fully dependent on the persons who are using it. So, business policy of each organization affects rules and regulation of applying management accounting.

2. Increase in Efficiency

It is the nature of management accounting that it is used for increasing in the efficiency of organization. It scans the points of inefficiency through analysis of accounting information. By taking action for improving, organization can increase the efficiency.

3. Supplies Information not Decisions

Management accountant supplies accounting facts and information and also provides interpretation, but decision making is fully dependent on higher authorities. Management accounting is just guide.

It is the temperament of management accounting that it is fully concerned with forecasting. In management accounting, historical accounting information is analyzed through common size financial statement, ratio analysis, fund flow analysis and accounting data tendency for knowing the probability of next fact. So, all these things are especially useful for forecasting.

These forecasting may be related with following things

a) sales forecasting

b) production forecasting

c) earning forecasting

d) cost forecasting

SCOPE:

Management Accounting Scope can be divided in following three parts

1. Analysis of Financial Statements Scope

2. Interpretation Scope

3. Decision Making Scope

Now we explain all above parts with more detail.

1. Analysis of Financial Statements/Accounting Data Scope

This part of management accounting scope answers our following questions

Q:- Which tools are being used for analyzing of accounting data?

Q:- Which specific accounting data is used for analyzing financial position, income position and solvency position?

Q:- What are main types of financial statement analysis?

Q:- What are the limitations of financial statement analysis?

2. Interpretation Scope

After analysis through ratio analysis, fund flow analysis, cash flow analysis or any other tool of management accounting, our next management accounting scope is interpretation scope. Analyzed data is also no tongue if you have no idea how to explain it? So, this is big scope for every wise man. Same analyzed financial statement's meaning may be different if interpretation is given by different account managers. For example, If we open the financial statement of twelve five years plan and we find that govt of India paid 1,10,000 Crores rupees for ending of poverty and you can find different detail of it. But if new account manager links it with no. of poor people, then we can see still 85% persons are poor. So, meaning of spending of Rs. 1,10,000 crores will become opposite. So, interpretation is important part of management accounting scope.

3. Decision Making Scope

"Who and how is the accounting information used for decision making?", is the part of scope of management accounting.

FUNCTIONS OF MGT ACCOUNTING:

Management accounting is one of important part of accounting. To use accounting for decision making encourages its development. Management accounting’s main function is to collect accounting information which is useful for different managerial functions like planning, organization, coordination and control. Now, we are explaining other important functions of management accounting.

1st Planning and Forecasting Function:

In 2005, Mr. A started his small business. He was well educated of management accounting tools. By effective use of management accounting, he developed his small business. Now, after 5 years, he is operating good company. Management accounting’s basic functions like to study ratio analysis and cash and fund flow statements can develop any small business like Mr. A. How is it possible?

One – Businessman can easily watch in which project he invested his cash and fund. He can see whether its ROI and ROE is better than any other investment.

Second – He also makes good plan to reduce his investment in that project whose return is not sufficient.

2nd Modification of Data Function:

Second good function of management accounting is to modify of raw accounting data. After this, businessman bids fair to effective use these modify data in business’s management. Management accounting can be used to classify every accounting item in different views. There are so many accounting software which can be helpful to show sale or purchase or any other accounting items according to production level, area, season, country, age or quality of debtors or creditors.

One Side, it will build up analytic approach of company and other side, it will be helpful to check up each and every accounting item from different angels.

3rd Interpretation Function:

It is also function of management accounting to do complete interpretation of financial analysis. It cuts down work burden of manager because management accountant supports him by providing fact and interpretation of financial data after its analysis.

4th Management Control Function:

Management control can be possible only with management accounting function. Management accounting uses responsibility accounting tool in which different cost, revenue and investment centers are made. Proper budget is maintained in each centre. Analysis of actual recorded performance is compared with standard performance and deviation is evaluated. This will be helpful to fix up wrong side of company’s decision promptly. Thus company can do smoothly management control.

5th Communication Function:

Management accounting puts together all useful accounting information with comparable past data for good communication with govt., bankers and investors.

ADVANTAGES OF MA:

Today, we will make clear the advantages of management accounting. After reading this, you will surely study all concepts of management accounting more deeply for becoming perfect in it.

Management accounting is needed in business because it has capacity to change the business performance and financial position. Please pay attention to the advantages of management accounting.

1st : Increase Efficiency :

Management accounting increases the efficiency of operation of company. Everything is done in management accounting with a scientific system for evaluating and comparing the performance. With this, we find deviations. We will take promotional decisions on this basis. Other employees will also be motivated with this because if their performance will be favourable, they get reward of this. Thus management accounting increases efficiency.

2nd : Maximizing the Profitability :

Using of management accounting's budgetary control and capital budgeting tool, company can easily succeed to reduce both operating and capital expenditures. After this, company can reduce its price and then company will receive super profits.

3rd : Simplify the Financial Statements

For taking different managerial decisions, management accountant provides deep technical reports with simple interpretations in which he mentions the facts of financial statements, after this, company's management officers understand what is in financial statement and how will they use this for company's progress.

4th : Control of Business's Cash Flow :

It is one of important advantage of management accounting that it can be used for controlling of business's cash flow. We all know that cash in hand is better than in fixed properties if there is emergency to pay our loan or debt. So, management accountant deeply studies from where is money coming and where is it going. To check on misuse of money will surely control of business's cash flow.

5th : Business-critical Decisions

To take business - critical decisions, now management accounting will become more powerful. Global management accountants are coming for join on one plate-form for taking all business critical decisions.

TOOLS OF MA:

In previous educational contents, we've explained functions and advantages of management accounting. Both contents were published to tell the importance of this branch of accounting. We want to take this conversation a step further today, and discuss tools and techniques of management accounting that can be helpful to management for providing best information. Take a look at some of best tools and techniques of management accounting outlined below:

1st Tool : Analysis of Financial Statements

Analysis of financial statements is the main tool of management accounting. In this tool, we collect four financial statement, one is profit and loss account, second is balance sheet, third is cash flow statement and fourth and last is fund flow statement. After this, we calculate more than 30 ratios and also analyze the financial statement by financial analysis, fund flow analysis and cash flow analysis. Main aims of analysis of financial statements are following :

1. Profitability - its ability to earn income and sustain growth in both short-term and long-term. A company's degree of profitability is usually based on the income statement, whichreports on the company's results of operations;

2. Solvency - its ability to pay its obligation to creditors and other third parties in the long-term;

3. Liquidity - its ability to maintain positive cash flow, while satisfying immediate obligations;

Both 2 and 3 are based on the company's balance sheet, which indicates the financial condition of a business as of a given point in time.

4. Stability- the firm's ability to remain in business in the long run, without having to sustain significant losses in the conduct of its business. Assessing a company's stability requires the use of both the income statement and the balance sheet, as well as other financial and non-financial indicators.

2nd Tool : Budgetary Control

This is that tool of management accounting in which we make budgets for planning and control of fund. All budgets are made with past historical accounting data and future expectations. After this budgeted data is compared with actual recorded accounting data and performance is calculated on the basis of deviation between actual and expected performance.

3rd Tool : Decision Accounting

There are lots of decision which businessman has to take on the basis of tools of management accounting. One of management accounting tool is decision accounting. It is helpful to take main decision which we can explain following ways :

a) To Buy or to construct any fixed asset

b) Do's or Dont's to do any business activity

c) To choose best alternative

d) Calculation the price of product

Throughput Accounting (TA) is a dynamic, integrated, principle-based, and comprehensive management accounting's tool that provides managers with decision support information for enterprise optimization. Actually this is the extension of decision accounting. Throughput accounting is relatively new in management accounting. It is an approach that identifies factors that limit an organization from reaching its goal, and then focuses on simple measures that drive behavior in key areas towards reaching organizational goals.

5th Tool : MIS

We MIS tool, management accountant provides information needed to manage organizations effectively

. If we have to understand MIS, we need to understand ERP, SCM, CRM, DSS and other computer techniques for providing information with effective ways.

6th Tool : Financial Policy

Financial policy is that tool of management accounting which is needed to make good structure of capital mix We decide the proportion of share capital and loans in capital structure. Financial and operating leverages are also its sub-tools.

7th Tool : Working Capital Management

With this tool of management accounting, we manage short term assets and short term liabilities. All cash management, debtor management and inventory management will include in working capital management. We make also working capital cycle for knowing the firm's ability to convert its resources into cash. If there is low time for conversion of raw material into sales and then cash from debtor, it is good indication.

DIFF BETWEEN FINANCIAL ACCOUNTS AND MANAGEMENT ACCOUNTS:

Financial Accounting and Management accounting both are the main branches of Accounting. Both are very necessary for better business decision. All the data which is used in management accounting are taken from financial accounting. But there are many difference between financial accounting and management accounting.

Following are the main differences of financial accounting and management accounting :-

| Basis of Difference | Financial Accounting | Management Accounting |

| 1. Objectives | - In this, we record all the transactions. We make financial statements. | - In this, we analyze the financial statement through ratio analysis, fund flow statement and other tools. |

| 2. Nature | - Financial accounting is related to record of historical transactions. | - Management accounting is the presentation of data for future planning. We can also use estimated data in it. |

| 3. Subject-Matter | - In financial accounting, we find the financial statement of whole organization. | - In management accounting, we tries to best for finding each department's financial results and performance. |

| 4. Compulsion | - As per law, to make the financial statement by follow the financial accounting rules is necessary for companies. | - There is not any law compulsion for analyze the financial statement by following management accounting rules. It is just need for management planning. |

| 5. Reporting | - Financial accounting's reports are very useful outside interested parties like investors, bankers, govt. org. and creditors. | - Management accounting's reports are useful for inside management team for better decision making. |

| 6. Description | - All the transaction which we can measure in the money, will be recorded in financial accounting. | - All the records and events which are useful for managerial decision making, will be used for analyze. |

| 7. Accounting GAAP | - There are common GAAP in financial accounting which any accountant should follow. | - There is not any common GAAP for management accounting. Recently, management accountants are starting to follow rule of thumb. |

| 8. Period | - Financial statements in financial accounting are made for one financial period. | - There is not necessary for making analyze on the basis of one year data. We can use more than one year data in management accounting. For example trend analysis, we use 5 years or more data. |

| 9. Publication | - As per law, there is necessity to publish the financial statements in newspaper. | - Management Accounting's reports are personal and confidentially used for management's planning. |

| 10. Audit | - As per law, audit of financial statements are necessary which are made in financial accounting. | - As per law, there is not need of audit of management accounting reports. |

Financial Accounting Vs Cost Accounting

Both cost accounting and financial accounting are the parts of accounting. Both provide useful information to the businessman for decision making. Both can be used for reducing cost and increasing the profit and wealth of business. But there are lots of differences between cost accounting and financial accounting. Financial accounting provides the information of expenses on the basis of historical transactions. In cost accounting, we show the detailed information of expenses.

For example: We have 5 products. Financial accounting's income statement will show just the total material cost, direct expenses, indirect expenses, sale and net profit but it will not show the each product's material cost, labour cost, overhead cost, sale and net profit. All these information can be obtained through cost accounting.

Now, we are explaining the differences between cost accounting and financial accounting.

1. Meaning

Cost Accounting : Cost accounting is that part of accounting which is helpful to calculate the cost and control the cost. In cost accounting, we deeply study the variable cost, fixed cost, overheads and capital cost.

Financial Accounting : Financial Accounting is that part of accounting in which we record the transactions and we make the financial statements. Through making the financial statement, it provide information of profitability and financial position to the interested parties.

2. Objective

Cost Accounting : We can not take all decisions on the basis of information which have been provided by financial accounting. After making the financial statements under financial accounting, we calculate the cost of each unit and use the techniques of cost accounting for better decision making.

Financial Accounting : Main objective of financial accounting is to show the financial statement correctly.

3. Law

Cost Accounting : There is not any restriction on the cost accounts. It can be made according to the need of company but some company must audit their cost accounts under cost audit.

Financial Accounting : In financial accounting, there are lots of law restrictions. For example, company accounts and financial statements must be according to the format of company law. It should also follow the rules of IFRS and income tax law.

4. Controlling

Cost Accounting : In cost accounting, we study the techniques of controlling the cost. All the costs are calculated for the purpose of controlling the cost. For example, Company produces product A, B and C. If product C is generating 30% but product A and B is generating just 5%. We will try to control the cost of A and B product through different techniques of cost control.

Financial Accounting : In financial accounting, we just record the transactions correctly. We do not care to control the cost.

5. Profit Analysis

Cost Accounting : In cost accounting, to find the profit per job or per batch or per service unit is possible.

Financial Accounting : In financial accounting. we make the income statement which shows the net profit or loss or whole organisation not one job or batch.

6. Record

Cost Accounting : In cost accounting, both actual transactions record and estimations are used. For example budgetary control and variance analysis, we set the standard cost which is based on the estimations. These estimations may be differ from actual cost.

Financial Accounting : In financial accounting, we use actual transaction for recording purpose. We do not use the estimation for preparing income statements and balance sheet.

7. Valuation of Inventory

Cost Accounting : In cost accounting, inventory's valuation will be on cost.

Financial Accounting : In financial accounting, inventory's valuation will be on the cost or market value which will be low.

8. Cycle

Cost Accounting : In cost accounting, we first calculate the raw material cost. Then, we calculate the labour cost. Then, we calculate the direct material cost. After this, we calculate the overhead cost. All these cost are added. A profit margin is added. An estimated sale price is calculated. Its whole controlling cycle will be relating to control the cost of raw material, labour cost and overheads.

Financial Accounting : In financial accounting, we pass the journal entries. Then, we make the ledger accounts. Then, we prepare the trial balance. Then, we make the final accounts.

FINANCIAL STATEMENTS:

Financial statements are the final product of accounting and these statements show the balance sheet and profit and loss account of company. Financial statements are the base of decisions which are taken by management of company and other interested parties. All other interested parties include investors, creditors, customers, employees, future investors, government and public. They take decisions according to the results of these financial statements.

Features of Financial Statements

1. Recorded Facts

It is the feature of financial statements that it is based on recorded facts. We record daily transactions relating to cash, bank, purchase, sale and many others. All these transactions are recorded on the historical cost or revenue. So, financial statement shows only book value of assets, liabilities, incomes and expenditures.

2. Accounting Conventions

For making financial statements, we use some of accounting conventions. These conventions are useful for making financial statements more comparable, easy and real.

3. Accounting assumptions

For making financial statements, we accept going concern and measurement in money assumption.

4. Personal Judgment

Personal judgment is very important in making of financial statement. For example, if we use FIFO for valuation of inventory, our financial statements show result according to this judgment and it will different if we use LIFO for valuation of inventory. There are many other valuation methods and one of these; we have to apply in accounting. Except these, there are many other decisions affect financial statements.

Types of Financial Statement

1. Balance Sheet

2. Profit and Loss Account

3. Profit and Loss Appropriation Account

3. Fund Flow Statement

4. Cash Flow Statement

BALANCE SHEET:

Preparation of balance sheet of company is very necessary, because Indian Company law 1956 gives strict instruction about the format of balance sheet of a company. A company can make balance sheet according to the form given in Part I of schedule VI of company law 1956. A company can also make balance sheet summary form, but it has to attach its schedule in which explanation of different components are given. We are explaining different components of balance sheet of company which will be helpful for students to prepare balance sheet of company.

[* Remember the form of balance sheet under Section 211]

You should remember balance sheet and its all components thoroughly. It can be made either horizontal or vertical form. But total of assets should be equal to total of liabilities. Here, I am explaining these components.

Assets Side of Balance Sheet

Assets are written in right side of company’s balance sheet. In these assets, we include.

We will show all fixed assets which are purchased and used in business. This is the long term expenditure of company. In these assets, we will include following.

I) Land

II) Building

III) Plant and Machinery

IV) Furniture and Fixture

V) Leasehold assets

VI) Development of property

VII) Vehicles

VIII) Live stocks

IX) Railway sidings

We also include intangible assets in fixed assets head. Following are the main examples of intangible assets.

I) Goodwill

II) Patents

III) Trade marks and design

Depreciation is charged on every fixed asset except land, because value of land will increase after some time. Here, students are given advice that they should calculate the value of net fixed assets, if different fixed assets are purchased or sold during the year. The following table will be the part of working note.

Investment is outflow of fund for getting interest or dividend earning. So, it is the asset of company and will include in assets side. The following are the main investments.

a) Investment in Government or trust securities.

The following points must be kept in mind while you are showing investment in balance sheet.

i) Investment in fully paid up shares must be shown separately from investment in partly paid up shares.

ii) Investment in the form of shares in subsidiary company must be shown separately from investment in any other company.

c) Investment in immovable properties.

d) Investment in the capital of partnership firms.

Investment will be shown on cost or market value which is less.

3. Treatment of current assets , loan and advances in balance sheet

Current assets will be shown in separate head and following components will be included in it.

i) Stock in trade

ii) Work in progress

iii) Stock of stationary

iv) Stock of loose tools

v) Stock of stores and spare parts

a) With schedule bank

b) With other banks

The amount which is given by company to others in the form of loan or advances will be shown in asset side. Followings are its main examples.

a) Advance and loan to subsidiary company

b) Advance and loan to partnership firm

c) Bill of exchange / Bill receivables

d) Advance expenses paid

e) Outside incomes.

4. Miscellaneous expenditures

Expenses which are not written off will be shown in asset side of balance sheet. There is no market value of these expenses. Examples are given below.

i) Preliminary expenses

iii) Discount allowed on issue or shares and debentures

v) Development expenditure

5. Profit and Loss Account

If company suffers net loss after adjusting all reserves, then it will be shown in asset side. This amount can be also deducted from reserves in liabilities side. That time, we will not show it in asset side.

Liabilities Side of Balance Sheet

Liabilities Side of Balance Sheet

Liabilities are written in left side of company’s balance sheet. In these liabilities, we include.

2. Reserves and Surplus

Following reserves will be shown in liabilities side of balance sheet of company.

i) Capital reserves

ii) Share premium account

iii) Other reserves

v) Sinking fund

3. Secured Loan

If any loan is taken by company after keeping any asset as security, then it will be shown in secured loan head. Its detail is given below.

i) Debentures

ii) Loan and advances from subsidiaries

iii) Other loan and advances

iv) Interest payable on secured loan

4. Unsecured loan

Following will be the unsecured loan.

i) Fixed deposits of public

ii) Short term loans and advances

iii) Other loans

5. Current Liabilities and Provisions

All liabilities which is payable within one year, will be included in current liabilities head.

A) Current Liabilities

i) Acceptance or bill payables

iii) Interest payable other than on loan

B) Provisions

ii) Proposed dividend

iv) Provision for insurance, pension and other staff benefit schemes

v) Other provisions

6. Contingent liabilities

These types of liabilities will not be shown in balance sheet. But a simple footnote is made for its detail. Following may be the contingent liabilities of company.

ii) Uncalled liability on shares paid

iii) Areas of fixed cumulative dividends

iv) Any other contingent liability of company

PROFIT AND LOSS ACCOUNT:

I am giving simple proforma of profit and loss account and balance sheet of a businessman or sole trader. Making sole trader's final accounts proforma is very easy. You can even make it in your ms excel sheet without any help. It is in verticle form and net profit is shown on basis of general formula of accounting. You can make balance sheet because it is easy than making the balance sheet of company.

![]()

PROFIT AND LOSS APPROPRIATION ACCOUNT:

Profit and Loss Appropriation account is the part of financial statements of company. It is different from profit and loss appropriation account of partnership firm . When a company makes his profit and loss account, its net profit is transferred to the credit side of profit and loss appropriation account. Profit and loss account shows only the net profit or net loss from operation of business but profit and loss appropriation accounts shows all non- operational adjustment which is needed for proper distribution of net profit between shareholders and company for future growth.

So, net profit of P/L A/c is used for providing reserve, dividend, dividend distribution taxand adjustment of income tax.

In the debit side of this account, we will show the following items.

1. Transfer to reserve /general reserve.

2. Transfer to dividend/interim dividend/proposed dividend.

3. Debenture redemption fund account.

4. Dividend equalization fund account.

5. Dividend Distribution Tax (A 15% dividend distribution tax and surcharge of 3% is paid by companies before distribution.)

6. Income tax for previous year not provided for.

7. Surplus transfer to balance sheet.

In the credit side of this account, we will show the following accounts

1. Balance of surplus of previous year.

2. Net Profit of this year.

3. Amount withdrawn from general reserve or any other reserve.

4. Provision such as income tax provision no longer required or excess of provision or refund of tax.

Cash flow analysis or cash flow statement analysis is the tool of finance. Like financial and ratio analysis cash flow analysis is also show the strength and weakness of business’s operation and investments and other financial activities. In cash flow analysis, we are interested to know the answer of following questions.

Q:-1 Is company capable to pay the creditors through the amount receivable from debtors?

Ans: For this, we can check the difference between a/cs receivables and account payables and if a/cs receivable is more than a/cs payable then it means, we are capable to pay our creditors.

Q: - 2. Accounting personnel, who need to know whether the organization will be able to cover payroll and other immediate expenses?

Ans. If there is existence of cash in business after paying current liabilities, then it is sure that we can pay our payroll and other immediate expenses out of balanced money.

Q: - 3 Is the company financially sound?

Ans. Every company’s financial strength can be estimated by checking its liquidity position. For this, it is very necessary to prepare cash flow statement which shows business’s cash inflows and cash outflows and difference will show closing balance of cash. If it is sufficient to pay all the liabilities of business, then I can exhort to you that company is fully financially sound.

Q:- 4. Give the its example.

Ans. After watching this example you can understand, we are anlyzing information that we can get from cash flow statement.

Study following Cash flow Statements with direct and indirect methods for deep study of cash flow analysis

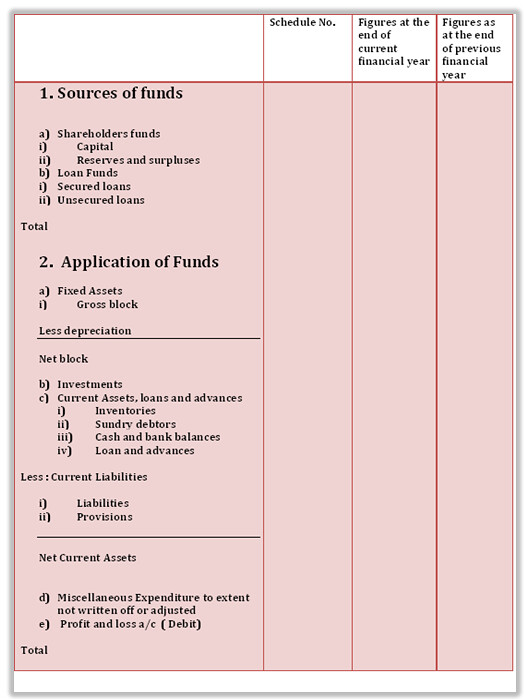

Vertical form of balance sheet does not demonstrate just financial position but it also shows the flow of fund in one year. We can create our balance sheet in such shape for knowing the exact position of our funds. If we include the previous figures of liabilities and assets, then we need not to make fund flow statement because to show the comparison of two period vertical balance sheets is just like fund flow statement. In short cut, it fulfills the requirement of fund flow analysis. One more mystery can be analyzed with this form of balance sheet. We can evaluate changes in working capital by comparing two vertical balance sheets.

Morover, most of the companies today use the vertical form for reporting because with this balance sheet looks without any clutter.

Now, we tell you the structure of vertical balance sheet. Basic formula is of accounting equation.

Capital + Liabilities = Assets

↓

Shareholder’s fund + long term liabilities + short term liabilities = Fixed assets + current assets

↓

Shareholder’s fund + Long term liabilities = Final Assets + Current Assets – Current Liabilities

↓

Source of Fund = Application of Fund

Morover, most of the companies today use the vertical form for reporting because with this balance sheet looks without any clutter.

Now, we tell you the structure of vertical balance sheet. Basic formula is of accounting equation.

Capital + Liabilities = Assets

↓

Shareholder’s fund + long term liabilities + short term liabilities = Fixed assets + current assets

↓

Shareholder’s fund + Long term liabilities = Final Assets + Current Assets – Current Liabilities

↓

Source of Fund = Application of Fund

Financial statements let you show the financial position and performance of company without checking each and every recorded transaction of company. This is also the best cause of your using financial statements before dealing with any company. This cause can help you save time and money to investigate each transaction when you are interested to invest your big money in any company, like US$100 million investment of Warburg Pincus in India’s NDR Group. After study financial statements of NDR Groups, Warburg pincus can easily understand whether NDR group's way of allocate resources good or bad. Whether invested assets in NDR group is performing well or not.

Now, we are explaining reasons of financial statements one by one:

1st Reason : Use of Balance Sheet :

This is the main financial statement. By study it, one side, we know list of different resources and what are different liabilities others have on those resources. Company can calculate, what % of assets from debt and what % of assets from equity? Each item of balance sheet is very useful to find large number of facts like current asset and current liabilities are useful for working capital position, reserves and surplus are useful for find security line of company etc. Moreover, we can compare balance sheet current year with previous year for finding increasing or decreasing trend of different assets and liabilities.

2nd Reason : Helpful For Ratio Analysis

Now, we are explaining reasons of financial statements one by one:

1st Reason : Use of Balance Sheet :

This is the main financial statement. By study it, one side, we know list of different resources and what are different liabilities others have on those resources. Company can calculate, what % of assets from debt and what % of assets from equity? Each item of balance sheet is very useful to find large number of facts like current asset and current liabilities are useful for working capital position, reserves and surplus are useful for find security line of company etc. Moreover, we can compare balance sheet current year with previous year for finding increasing or decreasing trend of different assets and liabilities.

2nd Reason : Helpful For Ratio Analysis

Ratio analysis's total concept is based on financial statements. All accounting ratios show the relationship among different items of financial statement like return on assets ratio is relationship of profit and total assets and debt to assets ratio is relationship between total debt and total assets of company.

3rd Reason : Universal Use

Financial statement can be used by any body for any purpose. Owners and shareholders may use it to find their profit margin and security of their investment. If employees see high profitability which is showed in company's financial statement, they can decide to demanding more compensation, promotion and rankings. Investors can use financial statement for taking their investment decisions. Creditors and lending companies can use financial statement for providing loan to company. Govt. can use financial statement for taking decision relating to taxes. Moreover, media's advertising rate is also affected from the trends of financial statement. If there is depression in industries due to any reason, financial statements of companies will show downward trend of sale and profit. At that time, media may decrease their advertising rates.

4th Reason : Market Value of Company

At the time of merge, market value of company is calculated on the basis of book value of company which is showed by financial statements.

3rd Reason : Universal Use

Financial statement can be used by any body for any purpose. Owners and shareholders may use it to find their profit margin and security of their investment. If employees see high profitability which is showed in company's financial statement, they can decide to demanding more compensation, promotion and rankings. Investors can use financial statement for taking their investment decisions. Creditors and lending companies can use financial statement for providing loan to company. Govt. can use financial statement for taking decision relating to taxes. Moreover, media's advertising rate is also affected from the trends of financial statement. If there is depression in industries due to any reason, financial statements of companies will show downward trend of sale and profit. At that time, media may decrease their advertising rates.

4th Reason : Market Value of Company

At the time of merge, market value of company is calculated on the basis of book value of company which is showed by financial statements.

Hey thanks for sharing this link to download the accounting eBook. I was in a great need of accounting book. Well dear, also share the link to download “Pricing of Initial Audit Engagement”- a publication of Dr. Aloke Ghosh!!

ReplyDeleteI appreciate how you broke down complex concepts into simple, understandable terms. Kudos! , Also Read Our Blog Post Financial Analysis Tools and Techniques

ReplyDelete