CAPITAL BUDGETTING :

PAYBACK PERIOD:

Author of AccountingCoach.com, Prof. Harold has given following two examples which guide as simple steps of calculating payback period. I have added these two examples as quote in Accounting Education.

Let's assume that a company invests $400,000 in more efficient equipment. The cash savings from the new equipment is expected to be $100,000 per year for 10 years. The payback period is 4 years ($400,000 divided by $100,000 per year).

A second project requires an investment of $200,000 and it generates cash as follows: $20,000 in Year 1; $60,000 in Year 2; $80,000 in Year 3; $100,000 in Year 4; $70,000 in Year 5. The payback period is 3.4 years ($20,000 + $60,000 + $80,000 = $160,000 in the first three years + $40,000 of the $100,000 occurring in Year 4).

Note that the payback calculation uses cash flows, not net income. Also, the payback calculation does not address a project's total profitability. Rather, the payback period simply computes how fast a company will recover its cash investment.

PAYBACK PERIOD:

Author of AccountingCoach.com, Prof. Harold has given following two examples which guide as simple steps of calculating payback period. I have added these two examples as quote in Accounting Education.

Let’s assume that a company invests $400,000 in more efficient equipment. The cash savings from the new equipment is expected to be $100,000 per year for 10 years. The payback period is 4 years ($400,000 divided by $100,000 per year).

A second project requires an investment of $200,000 and it generates cash as follows: $20,000 in Year 1; $60,000 in Year 2; $80,000 in Year 3; $100,000 in Year 4; $70,000 in Year 5. The payback period is 3.4 years ($20,000 + $60,000 + $80,000 = $160,000 in the first three years + $40,000 of the $100,000 occurring in Year 4).The payback period is calculated by counting the number of years it will take to recover the cashinvested in a project.

Let's assume that a company invests $400,000 in more efficient equipment. The cash savings from the new equipment is expected to be $100,000 per year for 10 years. The payback period is 4 years ($400,000 divided by $100,000 per year).

A second project requires an investment of $200,000 and it generates cash as follows: $20,000 in Year 1; $60,000 in Year 2; $80,000 in Year 3; $100,000 in Year 4; $70,000 in Year 5. The payback period is 3.4 years ($20,000 + $60,000 + $80,000 = $160,000 in the first three years + $40,000 of the $100,000 occurring in Year 4).

Note that the payback calculation uses cash flows, not net income. Also, the payback calculation does not address a project's total profitability. Rather, the payback period simply computes how fast a company will recover its cash investment.

RATE OF RETURN:

Rate of return is the method of capital budgeting. This method is used to select a goodinvestment project out of large number of investment projects. Under this method, we calculate rate of return. If we divide average net profit after depreciation and tax with the amount of investment and multiply with 100, then this will be rate of return and it will be compared with other projects’ rate of return. We only invest our money in that project whose rate of return will be high. If there is only one project, then we can compare its standard rate of return or minimum rate of return. This minimum rate is calculated by financial consultant after analyzing different investment.

We can calculate rate of return with following way:-

1st Way

Calculation of Average rate of return

2nd Way Average rate of return on average investment

In this way, firstly, we calculate average investment by dividing total investment by 2 because after dividing 2, the received average amount will equal to the amount which we can calculate after aggregating balance amount of investment after depreciation charging and then divided by number of years. So, it is easy to calculate just by dividing total investment by 2.

Now we can calculate average rate of return on average investment by following formula

For Example

Suppose, a company wants to buy $ 10 million machine and company can only invest in this project if minimum return on investment will receive 10 %. It is estimated that machine will give net profit after tax and depreciation $ 2 million. So rate of return is = 2/10 X 100 = 20% which is more than minimum return on investment. So, to invest in this project is profitable and company can accept this.

Rate of Return V/s Pay back period

Rate of return and pay back period are both traditional methods of capital budgeting in which we ignore the time value of money but rate of return method is better than pay back period because pay back period is the method in which Investor will accept only that project for the purpose of investment whose pay-back period is least out of different alternatives of projects. Other projects will be rejected. But overall profitability is not checked in this method. But rate of return method checks the overall profitability on the investment. We accept only that investment proposal whose rate of return is high and rate or return is also ROI. So, I think use of rate of return on investment is better for evaluation of investment proposals.

We can calculate rate of return with following way:-

1st Way

Calculation of Average rate of return

2nd Way Average rate of return on average investment

In this way, firstly, we calculate average investment by dividing total investment by 2 because after dividing 2, the received average amount will equal to the amount which we can calculate after aggregating balance amount of investment after depreciation charging and then divided by number of years. So, it is easy to calculate just by dividing total investment by 2.

Now we can calculate average rate of return on average investment by following formula

For Example

Suppose, a company wants to buy $ 10 million machine and company can only invest in this project if minimum return on investment will receive 10 %. It is estimated that machine will give net profit after tax and depreciation $ 2 million. So rate of return is = 2/10 X 100 = 20% which is more than minimum return on investment. So, to invest in this project is profitable and company can accept this.

Rate of Return V/s Pay back period

Rate of return and pay back period are both traditional methods of capital budgeting in which we ignore the time value of money but rate of return method is better than pay back period because pay back period is the method in which Investor will accept only that project for the purpose of investment whose pay-back period is least out of different alternatives of projects. Other projects will be rejected. But overall profitability is not checked in this method. But rate of return method checks the overall profitability on the investment. We accept only that investment proposal whose rate of return is high and rate or return is also ROI. So, I think use of rate of return on investment is better for evaluation of investment proposals.

PRESENT VALUE"

Today, we will learn a very important topic and its name is present value. If you invest in any investment proposal. Suppose, if you want to invest your money in machinery. There are many alternatives in the market. But you are seeing which is the best and which gives you better return. For this, you will calculate net present value (NPV) of cash flows of both machines. You should purchase only that machine that has high NPV. So, first of all we should know what present value is. Present value is the today value of future money.

Suppose, you have to invest your 100$ in Govt. bank. After one year, it will become $110 with 10% interest rate. So, $110's present Value is $ 100. Because, after one year, $100 will convert $ 110.

We can calculate present value of any amount with any discount rate with simple formula

PV = Amount / (1+r)

The present Value for all the cash inflows for a number of years is thus found as follows.

Suppose, you have to invest your 100$ in Govt. bank. After one year, it will become $110 with 10% interest rate. So, $110's present Value is $ 100. Because, after one year, $100 will convert $ 110.

We can calculate present value of any amount with any discount rate with simple formula

PV = Amount / (1+r)

The present Value for all the cash inflows for a number of years is thus found as follows.

{ Note: A1, A2, A3……… An are future net cash flows

r = rate of interest

2, 3 ……… n are number of years}

CUT OFF RATE:

Cut off rate is the minimum rate which will be received by investor, if he invests his money. It is just like cost of capital or return oninvestment. But it is not sure that investor will invest his money at cut off rate because, investor will deeply analyze his investment proposals with different capital budgetingtechniques. One of important technique is IRRin which cut off rate is compared with internal rate of return and if any project’s IRR will more than cut off rate, then that project will be accepted.

Many other techniques like NPV and P.I. in which we use cut off rate for calculating the present value of cash outlay and cash inflows.

Following are the major factors which affects cut off rate's determination :-

1. Amount of Investment

Cut off rate is the standard rate and it affects investment decisions. Amount of investment affects cut off rate’s determination. If investment amount is very high in any investment projects, then its cut off rate will be more than 10%.

2. Period of Investment

If any investment project offers to pay the amount of investment in installments, then cut off rate will be very small but if investor has to pay all amounts within one installment, then cut off rate may be very high.

3. Risk factor

If there is high risk with investment, then cut off rate will be high. If there is no risk of money, then investor can invest the money at very low cut off rate.

Many other techniques like NPV and P.I. in which we use cut off rate for calculating the present value of cash outlay and cash inflows.

Following are the major factors which affects cut off rate's determination :-

1. Amount of Investment

Cut off rate is the standard rate and it affects investment decisions. Amount of investment affects cut off rate’s determination. If investment amount is very high in any investment projects, then its cut off rate will be more than 10%.

2. Period of Investment

If any investment project offers to pay the amount of investment in installments, then cut off rate will be very small but if investor has to pay all amounts within one installment, then cut off rate may be very high.

3. Risk factor

If there is high risk with investment, then cut off rate will be high. If there is no risk of money, then investor can invest the money at very low cut off rate.

NET PRESENT VALUE:

Net present value method is that method of capital budgeting which is considered better than pay back period method and rate of return method for evaluation the investmentproposals or assets of different companies. In NPV method, we calculate net present value of cash flows after deducting present value of cash outflows from present value of cash inflows. This NPV is calcuated for each investment project. Only that investment project is accepted whose net present value will be high. Now, you can understand what is this method. In this method, I have used the term present value. Without knowing present value, you can not calculate net present value.

Simple Definition of Present Value and Value of Money

Present value means today value of one dollar. It is also value of money. Given money is one dollar. It may possible that value of one dollar may increase after one year because

#1. Receiving of Interest on one dollar for one year.

#2. Value of money may increase fluctuations in foreign exchange.

#3. Value of money may increase due to deflation in world market.

#4. Even in inflation, prices will increase and we need 2 dollar instead one dollar for buying same quantity. It means trend of value of money will always be upward.

So, today received one dollar is very important than what we receive tomorrow and Due to this reason, we fix a discount rate. It is the rate, which we like. At this rate, we want to invest our all money. On this rate, we can calculate present value of one dollar payable or receivable annually from present value table.

Simple Steps for calculating NPV

1st Step

To determine Discount Rate

This rate may be 8%, 9% or above according to financial market condition.

2nd Step

To calculate Present Value of Cash outflow or Initial Investment

It is calculated just by multiplying cash outflow with the present value of discount rate. If we invest today, then need not multiply because today investments means PV of Cash outflow.

3rd Step

To calculate the Present Value of Cash inflows or profit before depreciation and after tax

We can calculate PV of cash inflows by multiply present value of discount rate.

PV of Cash inflows = Cash inflows X Factor Value of Discount Rate

(For example, if we have to receive today 0.90 $ instead of $ 1. Then it will automatically $ 1 after one year, so if we multiply this 0.90 $ with Cash inflow, then cash inflow will become the amount which we receive today not in future. )

{Note: Present income is more important than future income}

4th Step

To Calculate Net Present Value

NPV = Present Value of Cash inflow – Present Value of Cash outflow

Calculation of NPV in Case Inflation

In case of inflation, we have to find real rate from nominal or discount rate and inflation rate.

In this section, I give you the introduction about how to get net present value of cash flows if inflation rate is given. It is very easy by using excel formula. Suppose, you have to buy machine of 10 million dollars. This is cash outflow and then after one year you have to receive cash inflows. For calculating net present value, you need real rate. If Nominal rate or discount rate is 11% and inflation is 5%, then you have to calculate real rate in excel sheet by using following formula.

Real rate = (1 + inflation rate ) / ( 1 + inflation rate) – 1

Now we calculate present value of cash inflow and present value of cash outflow on the basis of real rate.

Simple Definition of Present Value and Value of Money

Present value means today value of one dollar. It is also value of money. Given money is one dollar. It may possible that value of one dollar may increase after one year because

#1. Receiving of Interest on one dollar for one year.

#2. Value of money may increase fluctuations in foreign exchange.

#3. Value of money may increase due to deflation in world market.

#4. Even in inflation, prices will increase and we need 2 dollar instead one dollar for buying same quantity. It means trend of value of money will always be upward.

So, today received one dollar is very important than what we receive tomorrow and Due to this reason, we fix a discount rate. It is the rate, which we like. At this rate, we want to invest our all money. On this rate, we can calculate present value of one dollar payable or receivable annually from present value table.

Simple Steps for calculating NPV

1st Step

To determine Discount Rate

This rate may be 8%, 9% or above according to financial market condition.

2nd Step

To calculate Present Value of Cash outflow or Initial Investment

It is calculated just by multiplying cash outflow with the present value of discount rate. If we invest today, then need not multiply because today investments means PV of Cash outflow.

3rd Step

To calculate the Present Value of Cash inflows or profit before depreciation and after tax

We can calculate PV of cash inflows by multiply present value of discount rate.

PV of Cash inflows = Cash inflows X Factor Value of Discount Rate

(For example, if we have to receive today 0.90 $ instead of $ 1. Then it will automatically $ 1 after one year, so if we multiply this 0.90 $ with Cash inflow, then cash inflow will become the amount which we receive today not in future. )

{Note: Present income is more important than future income}

4th Step

To Calculate Net Present Value

NPV = Present Value of Cash inflow – Present Value of Cash outflow

Calculation of NPV in Case Inflation

In case of inflation, we have to find real rate from nominal or discount rate and inflation rate.

In this section, I give you the introduction about how to get net present value of cash flows if inflation rate is given. It is very easy by using excel formula. Suppose, you have to buy machine of 10 million dollars. This is cash outflow and then after one year you have to receive cash inflows. For calculating net present value, you need real rate. If Nominal rate or discount rate is 11% and inflation is 5%, then you have to calculate real rate in excel sheet by using following formula.

Real rate = (1 + inflation rate ) / ( 1 + inflation rate) – 1

Now we calculate present value of cash inflow and present value of cash outflow on the basis of real rate.

Internal rate of return is very advance method of capital budgeting and it is based on time value of money. Like NPV and P.I., we also calculate the present value of cash inflows and cash outflows in this method. But this method is purely different from NPV and PI. Before understanding this method of evaluation of investment projects , you should know what is internal rate of return.

Definition of Internal Rate of Return

If you have read the books of financial management of MBA or B.Com. class, you can give the definition of internal rate of return. Like other writers, I can also write that internal rate of return is the rate at which the present value of all cash inflows is equal to the present value of all cash outflows. After finding internal rate of return, we will accept that investment project whose internal rate will high or if there is only one project, then we will compare it with the minimum rate of return. If internal rate of return is more than cut off or minimum rate, then we will accept that single project.

Simplest Steps of Calculating Internal Rate of Return

Situation No. 1

When cash inflows are equal to the life of asset

First Step

If any asset will give equal return, then you can easily calculate present value factor by dividing initial cash outflow with the annual cash inflow.

Present Value Factor = Initial Investment cost / annual cash flow

Suppose initial investment cost = Rs. 50000

Life of the asset = 5 years

Estimated annual cash flow = Rs. 12500

Present Value factor = 50000/12500 = 4

Second Step

Then we will see present value annuity table and with this we can find the value of IRR.

As we see from the present value annuity table that 8% for 5 years period, the present value is 3.99 or approximately 4

So, internal rate of return is 8%

We will compare this rate with cut off or minimum standard rate of return and if this rate is more than minimum rate then this proposal will be accepted.

Situation No. 2

When the annual cash flows are unequal over the life of the assets and present value of cash inflows and cash outflows will equal at specific rate :-

Second situation is fully on the basis of hit and trial. This situation is like experiment in laboratory. Very few people know, I had worked in chemical science laboratory, where my boss scientist always made some mixture for invention and he ordered me to mix chemical and 90% his experiment failed but he did not loose his confidence. Like this, finance manager has to assume the rate. Suppose it may be 5%, 6% or more and then he has to find factor value of this rate and multiply it with the actual value of cash inflows and cash outflows. If both are equal at specific rate that that rate will be internal rate of return.

Situation No. 3

When the annual cash flows are unequal over the life of the assets and present value of cash inflows and cash outflows will equal between two rates :-

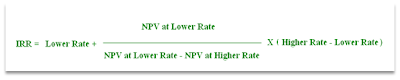

There is minimum chance of second situation where net present value will be zero. Some time present value of cash inflows may excess from present value of cash outflow or sometime cash outflow may excess from cash inflows, then we will calculate internal rate of return on the following simple formula

I have solved following question in screencast which also shows the steps of Situation No. 3

Definition of Internal Rate of Return

If you have read the books of financial management of MBA or B.Com. class, you can give the definition of internal rate of return. Like other writers, I can also write that internal rate of return is the rate at which the present value of all cash inflows is equal to the present value of all cash outflows. After finding internal rate of return, we will accept that investment project whose internal rate will high or if there is only one project, then we will compare it with the minimum rate of return. If internal rate of return is more than cut off or minimum rate, then we will accept that single project.

Simplest Steps of Calculating Internal Rate of Return

Situation No. 1

When cash inflows are equal to the life of asset

First Step

If any asset will give equal return, then you can easily calculate present value factor by dividing initial cash outflow with the annual cash inflow.

Present Value Factor = Initial Investment cost / annual cash flow

Suppose initial investment cost = Rs. 50000

Life of the asset = 5 years

Estimated annual cash flow = Rs. 12500

Present Value factor = 50000/12500 = 4

Second Step

Then we will see present value annuity table and with this we can find the value of IRR.

As we see from the present value annuity table that 8% for 5 years period, the present value is 3.99 or approximately 4

So, internal rate of return is 8%

We will compare this rate with cut off or minimum standard rate of return and if this rate is more than minimum rate then this proposal will be accepted.

Situation No. 2

When the annual cash flows are unequal over the life of the assets and present value of cash inflows and cash outflows will equal at specific rate :-

Second situation is fully on the basis of hit and trial. This situation is like experiment in laboratory. Very few people know, I had worked in chemical science laboratory, where my boss scientist always made some mixture for invention and he ordered me to mix chemical and 90% his experiment failed but he did not loose his confidence. Like this, finance manager has to assume the rate. Suppose it may be 5%, 6% or more and then he has to find factor value of this rate and multiply it with the actual value of cash inflows and cash outflows. If both are equal at specific rate that that rate will be internal rate of return.

Situation No. 3

When the annual cash flows are unequal over the life of the assets and present value of cash inflows and cash outflows will equal between two rates :-

There is minimum chance of second situation where net present value will be zero. Some time present value of cash inflows may excess from present value of cash outflow or sometime cash outflow may excess from cash inflows, then we will calculate internal rate of return on the following simple formula

In this formula we can also take the difference of PV at lower rate and Pv at higher rate. Both will give same answer.

I have solved following question in screencast which also shows the steps of Situation No. 3

MIRR:

PROFITABILITY INDEX:

Profitability Index has made his identity as the technique of evaluation of investmentprojects in financial market. This is fresh method and if any body has learnt NPV of capital budgeting, then he can also understand profitability index. In profitability Index, we also calculate the present value of cash outflows or investments for purchasing projects or assets and present value of cash inflows in the form of profit from investments. We use discount or minimum rate for calculating present value. After this profitability Index is calculated by dividing PV of cash inflows with PV of cash outflows.

P.I. = Present Value of Cash inflows / Present Value of Cash outflows

Profitability Index shows profitability, if we invest per unit of money. On the basis of profitability index, we can provide ranks to different investment projects. Higher P.I. will get higher rank and lower P.I. will get lower rank and only highest rank project will be accepted for real investment. If there is only one project and we have to decide whether investment in this project is profitable or not. This decision can be taken by calculating profitability index. If profitability index is one or more, then project should be accepted. A ratio of 1.0 is logically the lowest acceptable measure on the index. Any value lower than 1.0 would indicate that the project's PV is less than the initial investment. As values on the profitability index increase, so does the financial attractiveness of the proposed project.

NPV Vs Profitability Index

NPV method and profitability index are deeply connected with each other and both give same result for evaluation of investment projects. We accept that investment proposal whose NPV must be positive and we also accept that investment proposal whose P.I. must be more than one. If we compare two projects by applying both NPV and Profitability index and if NPV of first project is more than second project but Profitability index is less than second, at time, we will prefer first project because NPV will be capable to maximize the fund of shareholders.

P.I. = Present Value of Cash inflows / Present Value of Cash outflows

Profitability Index shows profitability, if we invest per unit of money. On the basis of profitability index, we can provide ranks to different investment projects. Higher P.I. will get higher rank and lower P.I. will get lower rank and only highest rank project will be accepted for real investment. If there is only one project and we have to decide whether investment in this project is profitable or not. This decision can be taken by calculating profitability index. If profitability index is one or more, then project should be accepted. A ratio of 1.0 is logically the lowest acceptable measure on the index. Any value lower than 1.0 would indicate that the project's PV is less than the initial investment. As values on the profitability index increase, so does the financial attractiveness of the proposed project.

NPV Vs Profitability Index

NPV method and profitability index are deeply connected with each other and both give same result for evaluation of investment projects. We accept that investment proposal whose NPV must be positive and we also accept that investment proposal whose P.I. must be more than one. If we compare two projects by applying both NPV and Profitability index and if NPV of first project is more than second project but Profitability index is less than second, at time, we will prefer first project because NPV will be capable to maximize the fund of shareholders.

CAPITAL RATIONING:

Capital rationing is technique which is used with capital budgeting techniques. Capital rationing technique is used when company has limited fund for investing in profitableinvestment proposals. In other words Capital rationing is a strategy employed by companies to make investments based on the current relevant circumstances of the company.

Explanation of Capital Rationing With Simple Example

For example, Company fixes his priority to invest his money in more profitable projects. Suppose a company has $ 1 million dollar and after using the Profitability index technique of capital budgeting company found that three projects of $ 600000, $ 300000 and $ 400000 are profitable out of seven projects but if company has limited cash of $ 1 million only. With this money, company can use capital rationing technique. Under this technique, if company sees that First and third proposal’s profitability index is high than second, then they will select only two projects combination out of three projects. Read also secondexample of capital rationing.

Explanation of Capital Rationing With Simple Example

For example, Company fixes his priority to invest his money in more profitable projects. Suppose a company has $ 1 million dollar and after using the Profitability index technique of capital budgeting company found that three projects of $ 600000, $ 300000 and $ 400000 are profitable out of seven projects but if company has limited cash of $ 1 million only. With this money, company can use capital rationing technique. Under this technique, if company sees that First and third proposal’s profitability index is high than second, then they will select only two projects combination out of three projects. Read also secondexample of capital rationing.

One of my UK student wants to know the capital rationing with simple example. before studying the example, please read following introduction of capital rationing.

Capital rationing exists when investor is interested to invest his limited fund in most profitable investment proposal. In this case, a firm may be confronted with more “desirable” projects than it is willing to finance.

Now, We can explain capital rationing more deeply with following simple example:

Capital Rationing: An Example: (Firm’s Cost of Capital = 12%)

Independent projects ranked according to their IRRs:

Project Project Size→ IRR

E $20,000→ 21.0%

B 25,000 →19.0

G 25,000→ 18.0

H 10,000→ 17.5

D 25,000 →16.5

A 15,000→ 14.0

F 15,000 →11.0

C 30,000 →10.0

No Capital Rationing - Only projects F and C would be rejected. The firm’s capital budget would be $120,000.

Existence of Capital Rationing - Suppose the capital budget is constrained to be $80,000. Using the IRR criterion, only projects E, B, G, and H, would be accepted, even though projects D and A's IRR is higher than our cost of capital but we can not include because of our capital budget is limited upto $ 80000.

{*Also note, however, that a theoretical optimum could be reached only be evaluating all possible combinations of projects in order to determine the portfolio of projects with the highest NPV.}

Capital rationing exists when investor is interested to invest his limited fund in most profitable investment proposal. In this case, a firm may be confronted with more “desirable” projects than it is willing to finance.

Now, We can explain capital rationing more deeply with following simple example:

Capital Rationing: An Example: (Firm’s Cost of Capital = 12%)

Independent projects ranked according to their IRRs:

Project Project Size→ IRR

E $20,000→ 21.0%

B 25,000 →19.0

G 25,000→ 18.0

H 10,000→ 17.5

D 25,000 →16.5

A 15,000→ 14.0

F 15,000 →11.0

C 30,000 →10.0

No Capital Rationing - Only projects F and C would be rejected. The firm’s capital budget would be $120,000.

Existence of Capital Rationing - Suppose the capital budget is constrained to be $80,000. Using the IRR criterion, only projects E, B, G, and H, would be accepted, even though projects D and A's IRR is higher than our cost of capital but we can not include because of our capital budget is limited upto $ 80000.

{*Also note, however, that a theoretical optimum could be reached only be evaluating all possible combinations of projects in order to determine the portfolio of projects with the highest NPV.}